Apple’s upcoming Pay Later service still doesn’t have an official release date, but more details have surfaced about how Apple will determine the ‘creditworthiness’ of its users.

Apple Pay Later is currently in a testing phase ahead of a public launch in the US, with many of its employees taking part in the trial. If you’ve been wondering what the approval criteria will be like for using Apple Pay Later, a report from Bloomberg reveals a little more about the lending process.

Apple’s lending criteria

It seems Apple will scrutinize a user’s digital history to calculate whether they’re a good prospect for lending. That means digging through whatever troves of data Apple ties to you, such as the apps and subscriptions you’ve paid for, your Apple Store purchases, and how much you use Apple Cash peer-to-peer payments. The report says that even the devices you own are taken into account, all in the name of working out whether you’re a ‘good’ customer.

Of course, Apple likes to boast about its dedication to user privacy, and all this digging through histories feels somewhat at odds with that. But it has to be reasonably sure a person will pay the money back, and Apple doesn’t have quite as much data to screen through as some other companies might. It doesn’t store your Apple Pay purchase history, for one – hence the reliance on things purchased directly from Apple instead of more general transactions. Here’s what Apple has to say on the matter:

“Apple doesn’t store or have access to the original credit, debit, or prepaid card numbers that you use with Apple Pay. And when you use Apple Pay with credit, debit, or prepaid cards, Apple doesn’t retain any transaction information that can be tied back to you— your transactions stay between you, the merchant or developer, and your bank or card issuer.”

So ultimately it looks as though a combination of Apple-related history – but not specific purchases – may be used to decide how much you can split through Apple Pay Later.

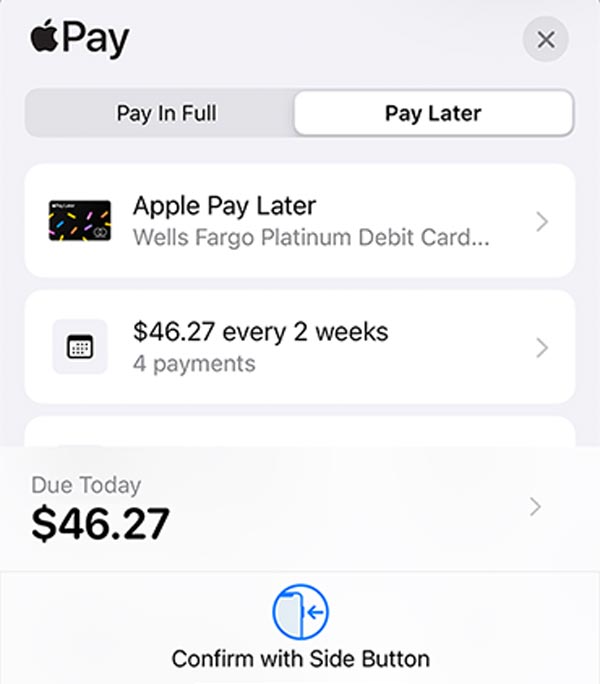

More on Apple Pay Later

The service, which allows Apple Pay users to split purchases into four payments across six weeks, was unveiled at WWDC last year and marks a somewhat unexpected move into financial services for Apple. Powered by the existing Mastercard network, Apple Pay Later “just works” with no additional integration required from merchants.

The feature will be built into the Wallet app, giving Apple Pay customers a way to spread out the cost of large purchases without incurring interest or transaction fees. The app will deal with tracking what’s owed and when it needs to be paid. With so many similar ‘pay later’ apps proving popular with customers, Apple has decided to ditch the middleman and offer an easier way for Apple Pay users to access it. Testers have reported being able to borrow up to $1000 as part of the Pay Later program.

Of course, as with any service like this – which is essentially a loan – missing those repayments can land you in trouble and prompt additional penalty charges.